As global markets grapple with cautious Federal Reserve commentary and political uncertainty, U.S. stocks have experienced a broad-based decline, raising investor concerns about the sustainability of recent market rallies. Amid these fluctuating conditions, identifying potentially undervalued stocks becomes crucial for investors seeking opportunities that may offer resilience and growth potential in an uncertain economic landscape.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Clear Secure (NYSE:YOU) | US$26.66 | US$53.14 | 49.8% |

| Sudarshan Chemical Industries (BSE:506655) | ₹1129.90 | ₹2252.82 | 49.8% |

| Hanza (OM:HANZA) | SEK76.20 | SEK151.92 | 49.8% |

| HealthEquity (NasdaqGS:HQY) | US$94.95 | US$189.22 | 49.8% |

| Aguas Andinas (SNSE:AGUAS-A) | CLP293.50 | CLP584.13 | 49.8% |

| Ingenia Communities Group (ASX:INA) | A$4.62 | A$9.19 | 49.7% |

| South Atlantic Bancshares (OTCPK:SABK) | US$15.02 | US$29.98 | 49.9% |

| KebNi (OM:KEBNI B) | SEK1.09 | SEK2.17 | 49.8% |

| RENK Group (DB:R3NK) | €18.342 | €36.50 | 49.7% |

| iFLYTEKLTD (SZSE:002230) | CN¥51.75 | CN¥103.29 | 49.9% |

Click here to see the full list of 875 stocks from our Undervalued Stocks Based On Cash Flows screener.

Underneath we present a selection of stocks filtered out by our screen.

Overview: Taiyo Yuden Co., Ltd. develops, manufactures, and sells electronic components in Japan, China, Hong Kong, and internationally with a market cap of ¥274.10 billion.

Operations: The company’s primary revenue segment is the Electronic Components Business, generating ¥335.08 billion.

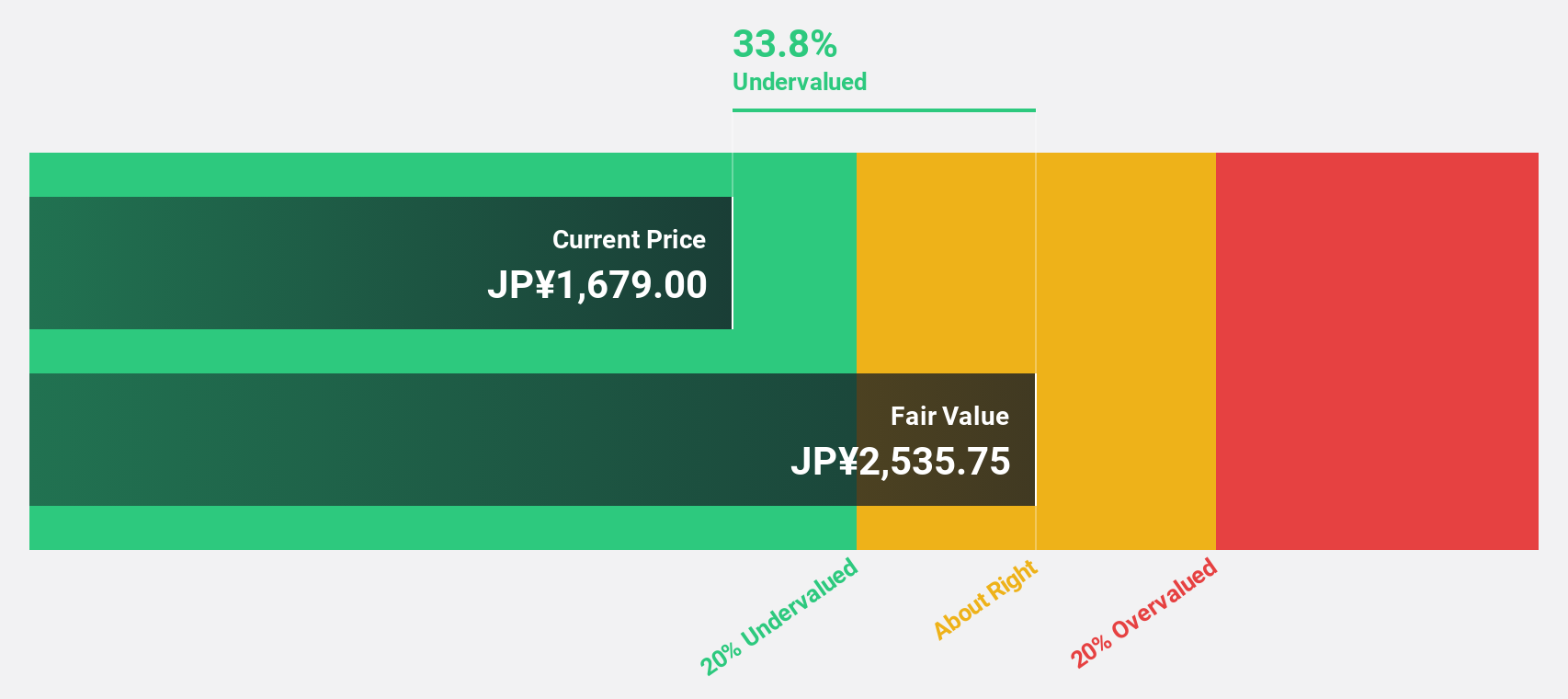

Estimated Discount To Fair Value: 38.3%

Taiyo Yuden is currently trading at ¥2,197.5, significantly below its fair value estimate of ¥3,560.2, indicating potential undervaluation based on cash flows. Despite earnings growth of 388.7% last year and a forecasted annual profit growth of 33.88%, recent corporate guidance lowered expectations for net sales and operating profits for the fiscal year ending March 2025 due to revised demand forecasts, impacting short-term financial outlooks negatively.

Overview: Relo Group, Inc. provides property management services in Japan and has a market cap of ¥292.71 billion.

Operations: The company’s revenue is primarily derived from its Relocation Business at ¥97.34 billion, followed by the Welfare Program at ¥26.52 billion and the Tourism Business at ¥15.17 billion.

Estimated Discount To Fair Value: 33.9%

Relo Group is trading at ¥1,955.5, significantly below its fair value estimate of ¥2,960.58, suggesting potential undervaluation based on cash flows. The company forecasts revenue growth of 5.6% annually and earnings growth of 18.69%, outpacing the market average with expected profitability in three years. However, its dividend yield of 1.94% lacks coverage by earnings. Recent share buybacks totaling ¥5,499.88 million reflect strategic capital management efforts to enhance shareholder value.

Overview: NFI Group Inc. manufactures and sells buses across North America, the United Kingdom, Europe, and the Asia Pacific with a market cap of approximately CA$1.67 billion.

Operations: The company’s revenue is primarily derived from Manufacturing Operations, which generated $2.46 billion, and Aftermarket Operations, contributing $610.03 million.

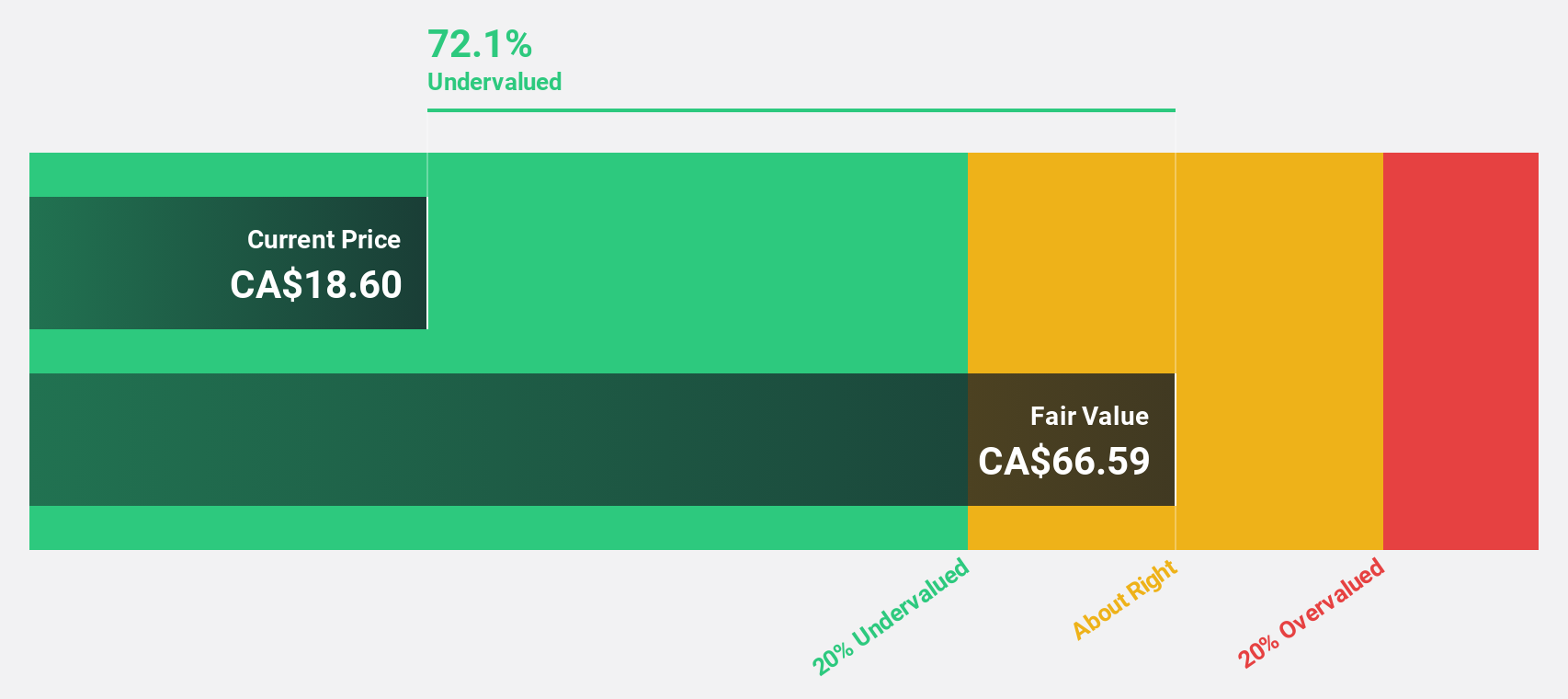

Estimated Discount To Fair Value: 44.1%

NFI Group is trading at CA$14.02, well below its estimated fair value of CA$25.09, indicating undervaluation based on cash flows. Despite lowered revenue guidance for 2024 to US$3.1-3.3 billion, the company shows improved financials with reduced net losses and growing sales year-over-year. Analysts anticipate a 49.8% rise in stock price and forecast annual revenue growth of 15.6%, surpassing Canadian market averages while expecting profitability within three years despite interest coverage concerns.

Next Steps

Ready To Venture Into Other Investment Styles?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice.

It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if NFI Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]