As global markets navigate a mixed start to the new year, with U.S. stocks finishing another strong year despite recent economic indicators pointing towards challenges, investors are increasingly on the lookout for opportunities that may be trading below their intrinsic value. In such an environment, identifying undervalued stocks can be crucial, as these investments have the potential to offer significant returns if market conditions align with their fundamental strengths.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Camden National (NasdaqGS:CAC) | US$42.01 | US$83.84 | 49.9% |

| Brickability Group (AIM:BRCK) | £0.626 | £1.25 | 49.8% |

| Decisive Dividend (TSXV:DE) | CA$6.00 | CA$11.94 | 49.8% |

| Brunel International (ENXTAM:BRNL) | €9.84 | €19.64 | 49.9% |

| Emporiki Eisagogiki Aftokiniton Ditrohon kai Mihanon Thalassis Societe Anonyme (ATSE:MOTO) | €2.73 | €5.44 | 49.8% |

| EnomotoLtd (TSE:6928) | ¥1452.00 | ¥2887.72 | 49.7% |

| Zhende Medical (SHSE:603301) | CN¥20.99 | CN¥41.91 | 49.9% |

| ReadyTech Holdings (ASX:RDY) | A$3.14 | A$6.25 | 49.8% |

| Neosperience (BIT:NSP) | €0.572 | €1.14 | 49.8% |

| Vogo (ENXTPA:ALVGO) | €2.92 | €5.81 | 49.8% |

Click here to see the full list of 890 stocks from our Undervalued Stocks Based On Cash Flows screener.

Here’s a peek at a few of the choices from the screener.

Overview: Vestas Wind Systems A/S is involved in the design, manufacture, installation, and servicing of wind turbines across the United States, Denmark, and internationally with a market cap of DKK105.39 billion.

Operations: The company’s revenue is derived from two main segments: Service, contributing €3.42 billion, and Power Solutions, which accounts for €12.51 billion.

Estimated Discount To Fair Value: 49.1%

Vestas Wind Systems appears undervalued based on cash flow analysis, trading over 20% below its estimated fair value of DKK205.06. Despite slower revenue growth forecasts at 9.3% annually, Vestas’ earnings are expected to grow significantly at 35.7% per year, outpacing the Danish market. Recent large-scale orders across Europe and North America highlight robust demand for its wind turbines, potentially bolstering future cash flows and supporting a positive investment outlook amidst volatile share prices.

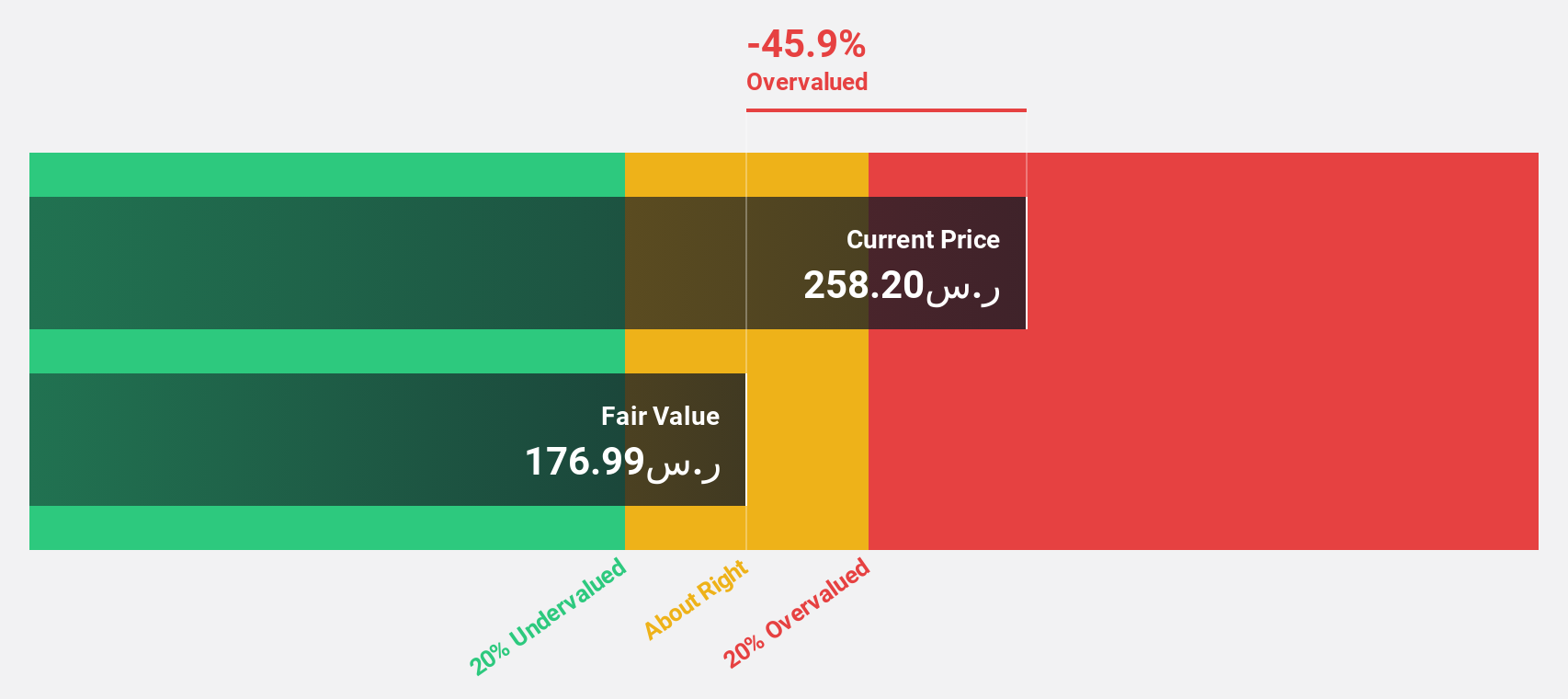

Overview: Dr. Sulaiman Al Habib Medical Services Group operates hospitals, medical complexes, day surgery centers, and pharmaceutical facilities in Saudi Arabia and internationally with a market cap of SAR101.64 billion.

Operations: The company’s revenue segments include SAR8.14 billion from hospitals and healthcare facilities, SAR2.22 billion from pharmacies, and SAR198 million from HMG Solutions.

Estimated Discount To Fair Value: 22.7%

Dr. Sulaiman Al Habib Medical Services Group is trading approximately 22.7% below its estimated fair value of SAR375.61, with a current price of SAR290.4, suggesting it may be undervalued based on cash flow analysis. The company’s earnings and revenue are forecast to grow at 14.9% and 14.8% annually, respectively, outpacing the Saudi Arabian market averages despite high debt levels and significant non-cash earnings impacting quality assessments. Recent leadership changes could influence strategic direction positively over the long term.

Overview: adidas AG, along with its subsidiaries, is involved in the design, development, production, and marketing of athletic and sports lifestyle products across Europe, the Middle East, Africa, North America, Greater China, the Asia-Pacific region, and Latin America; it has a market capitalization of approximately €43.44 billion.

Operations: The company’s revenue is derived from several key regions, including €3.34 billion from Greater China, €2.44 billion from Latin America, and €4.95 billion from North America.

Estimated Discount To Fair Value: 44.6%

Adidas is trading at €243.3, significantly below its estimated fair value of €439.09, highlighting potential undervaluation based on cash flows. The company’s earnings are forecast to grow robustly at 32.6% annually, surpassing the German market’s growth rate of 20.1%. Recent financial results show improved profitability with third-quarter net income rising to €443 million from €259 million year-over-year, reflecting strong operational performance despite slower revenue growth projections.

Taking Advantage

Ready For A Different Approach?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice.

It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Explore Now for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]